"...the amount of waiting involved in a particular investment is not simply proportional to the length of the investment period and the value of the input invested, but is dependent also on the rate of interest. In consequence, when we compare two different investment structures, it will not always be possible even to say, on purely technical grounds, which of them involves the greater amount of waiting. At one set of relative values for the different kinds of input and at one rate of interest, the one structure, and at a different set of values or a different rate of interest, the other structure, will represent the greater amount of waiting, or will be 'longer' in the sense in which this term has commonly been used." -- F. A. Hayek (1941). The Pure Theory of Capital, University of Chicago Press: 144I know about this quotation from Roger W. Garrison's article "Reflections on Reswitching and Roundaboutness".

Wednesday, February 28, 2007

Hayek On Reswitching

Monday, February 26, 2007

Richard Chase On Reswitching

"Thus the reswitching anomaly, along with its theoretical developments and implications, has been placed in abeyance. And so it must be, for if this criticism were taken as being no less applicable to the real world than the theoretical, then it follows, as already noted, that orthodox economics is unable to make any reliable statements concerning the relationship of production to the various input markets. That is, the neoclassical vision of a market-coordinated production system, along with derivative growth and distribution theories, are all invalidated. As a consequence, the nature of the entire traditional circular flow conception is called into question...

...It is one thing to say that this conception of indirect economic management does not satisfactorily achieve its goals because of the existence of such real-world problems as bottlenecks, power, premature inflation, inflationary expectations, random shocks, ratchet and spillover effects, and the like. In such situations, an economically coherent and consistent market-based system of production and distribution is still assumed to exist, though it is overlaid with political, institutional, and psychological factors that affect economic adjustments and performance. The basic strategy, in this case, would be to maintain the general neoclassical-synthetic emphasis on fiscal and monetary management (with perhaps somewhat greater stress on the monetary tool, if the monetarists were to have their way), and supplement these tools with finely targeted direct and specific devices - for example, stricter antitrust enforcement, more sharply focused incentive (and disincentive) taxes, expanded job training and subsidization programs - so as to allow and encourage the effective functioning of centerpiece fiscal and monetary devices.

It is quite another thing to argue that key markets in the system, particularly those in the resource or input sector, do not possess the fundamental economic characteristics necessary to the orderly systematic functioning that is postulated by mainstream theory..." -- Richard X. Chase, "Production Theory," in A Guide to Post-Keynesian Economics, (edited by Alfred S. Eichner), M. E. Sharpe, 1978, p. 79-80

Sunday, February 25, 2007

Diane Coyle for the Defense

"Would you agree with the following statement? '[Economists] should take credit for the deteriorating quality of existence. For it is their philistine notions of personal and national welfare that have helped to ruin the natural world; confused technology with culture; reduced art to money, time to interest, sexual relations to pornography, friendship to advantage, and liberty to shopping, and wasted whole generations who, because they have only been taught to think in categories of money, have, in Schopenhauer's phrase, "missed the purpose of existence".'What "whole generation of research" is Diane Coyle talking about? Presumably it would include literature making claims like the following:

If so, you'd have plenty of company...

...What is truly bizarre about this persistent and frequent set of claims - economics ignores or over-simplifies reality, is based on a false conception of human nature, is only about money, thinks the world operates like a machine - is how untrue it is. Those who make the claims haven't been reading any of the economics published since about 1980. The caricature never represented reality all that accurately, but a whole generation of research has made it completely unrecognisable..." -- Diane Coyle (2007). "Economics, the Soulful Science"

"One thing we have learned for sure as a consequence of this programme of research is that [Expected Utility Theory] is descriptively false. Mountains of experimental evidence reveal systematic (i.e., predictable, not random) violations of the axioms of EUT, and the more we look, the more we find. This is not good news for the general economist, but there it is." - Chris Starmer (1999). "Experimental Economics: Hard Science or Wasteful Tinkering?", Economic Journal, V. 109, N. 453 (February): F5-F15Somebody who is concerned to comment on the notion that economists "think the world operates like a machine" and emphasizes literature since, say, 1980 surely has read Philip Mirowski. (I'm fairly sure Deidre McCloskey and Paul Ormerod have, for example.) And I know Mirowski has read, for example, Starmer.

Mirowski is always quotable. Here are some quotations from one Mirowski essay:

"Because I am not a product of a successful socialization into the economics profession, lots of things that economists say strike me as funny. The idea we are paid according to our marginal productivity, for instance, rocks me as risible; the tendency to suggest the economy 'overheats' is a richly wrought satire. The doctrine that the market maximizes the freedom of a set of agents identical in all relevant respects is a joke worthy of Nietzsche...

...Asking me now to write on how I feel about economics journals is like asking a lamppost to write a memoir on dogs...

...when I read a particular economist's advocacy of regarding children as consumer goods, or another insists that Third World countries should be dumping grounds for toxic industrial wastes since life is cheap there, or a third proclaims that no sound economist would oppose NAFTA, or a fourth asserts confidently that some price completely reflects all relevant underlying fundamentals in the market, or a fifth pronounces imperiously that no credible theorist could recommend anything but a Nash equilibrium as the very essence of rationality in a solution concept, I do not view this as an occasion to dispute the validity of the assumptions of their 'models'; rather, for me, it is a clarion call to excavate the archaeology of knowledge which allows such classes of statements to pass muster, as a prelude to understanding what moral presuppositions I must evidently hold, given that I find them deeply disturbing..." - Philip Mirowski (1997). "Confessions of an Aging Enfant Terrible"

Friday, February 23, 2007

Wednesday, February 21, 2007

Roger Garrison, Correct to Mistaken

Roger Garrison knows that one concerned with the theory of interest better not be confused about units of measurement:

"The price of any factor is measured in terms of dollars per unit of the factor. Land rent is measured in $/(acre-year); the wage rate in $/(worker-hour); the service price of a capital good, say a machine, in $/(machine-hour). The interest rate is measured in frequency units, in inverse time. That is, the dimensions of the interest rate are 1/year - e.g. 10% per year. Any attempt to recast the interest rate as the price of a factor must be squared with this dimensional characteristic.And he knows the textbooks to be misleading to wrong:

It can be seen immediately that the interest rate cannot be the price - or even the service price - of capital goods. The dimensions of $/machine - or of $/(machine-hour) - are not the same as the units of the interest rate." - Roger Garrison (1988, p. 50)

"The Fisherian analytics are simple enough, but the basic construction is conceptually flawed. Again, the issue of dimensions comes into play. The slope of the indifference curves has the dimensions of the interest rate (1/year). The slope of the opportunity curve must be dimensionally the same if the point of tangency is to have any intelligible meaning at all. If the slope is a marginal value product, then it must be the marginal value product of waitings not of capital. But as demonstrated in the previous section, the quantity of waiting is itself dependent upon factor prices, which in turn are dependent upon the interest rate. It cannot legitimately be argued, then, that the rate of interest has two independent co-determinants; one of those co-determinants is dependent upon the magnitude it supposedly helps to determine.Garrison knows that dimensional analysis has implications about the theory of capital:

Modern textbook writers have attempted to skirt this problem by using a one-good model. In all such models, questions of value, which may be affected by changes in the rate of interest, simply do not arise. Value productivity and physical productivity are indistinct; productivity is modelled as the rate of increase in the quantity of the good. The phenomenon of interest is being analogized once again to sheep that reproduce or to plants that grow. But, as Professor Rothbard often reminds us, the rate of interest is a ratio of values, not of quantities. This modelling technique unavoidably conflates growth rates with interest rates and fails thereby to shed any light on the phenomenon of interest." - Roger Garrison (1988, p. 52-53)

"Suppose the current rate of interest (the price of waiting) is 5 per-cent and that the equilibrium quantity of waiting supplied and demanded is 1000 $-years, which consists of owning durable machines, whose current value is $1000, for one year. Now suppose that the demand for waiting increases. Simple supply-and-demand analysis would allow us to predict that the interest rate will rise, say from 5 to 10 percent, and that the quantity of waiting supplied and demanded will increase.Here Garrison is just wrong:

If the value of the machines could be assumed not to change, this prediction would be valid. But a rise in the interest rate will cause the value of the machines, which is simply the discounted value of the machines' future output, to fall. More specifically, the doubling of the rate of interest, which serves as the basis for the discounting, will cause the value of the machines to decrease from $1000 to $500. Owning those same machines for a year now constitutes only half the waiting. It is possible, then, that in the subsequent equilibrium, more machines will be owned for a longer period of time yet the amount of waiting, which is now based on a lower machine price, may be less than in the initial equilibrium." - Roger Garrison (1988, p. 51)

"There is no ambiguity, however, about the direction of change in the rate of interest given a particular shift in supply or in demand. An increase in the demand for waiting, which is the same thing as a rise in time preferences, will cause the rate of interest to rise." - Roger Garrison (1988, p. 51)

- Garrison, Roger W. (1988). "Professor Rothbard and the Theory of Interest", in Man, Economy, and Liberty: Essays in Honor of Murray N. Rothbard (edited by Walter Block and Llewellyn H. Rockwell, Jr.), Ludwig von Mises Institute

Monday, February 19, 2007

Hayek Versus Sraffa

I think Piero Sraffa talks his friend Friedrich Hayek into an absurd position here:

"Mr. Sraffa denies that the possibility of a divergence between the equilibrium rate of interest and the actual rate is a peculiar characteristic of a money economy. And he thinks that 'if money did not exist, and loans were made in terms of all sorts of commodities, there would be a single rate which satisfies the conditions of equilibrium, but there might, at any moment, be as many "natural" rates of interest as there are commodities, though they would not be equilibrium rates.' I think it would be truer to say that, in this situation, there would be no single rate which, applied to all commodities, would satisfy the conditions of equilibrium rates, but there might, at any moment, be as many 'natural' rates of interest as there are commodities, all of which would be equilibrium rates; and which would all be the combined result of the factors affecting the present and future supply of the individual commodities, and of the factors usually regarded as determining the rate of interest. There can, for example, be very little doubt that the 'natural' rate of interest on a loan of strawberries from July to January will even be negative, while for loans of most other commodities over the same period it will be positive." -- F. A. Hayek (1932)

"I have only a few words to add on the second cardinal question, that of the 'money' and the 'natural' rates of interest. Dr. Hayek's ideal maxim for monetary policy, like that of Wicksell, was that banks should adopt the 'natural' rate as their 'money' rate for loans... I pointed out ... that when saving was in progress there would at any one moment be many 'natural' rates, possibly as many as there are commodities; so that it would be not merely difficult in practice, but altogether inconceivable, that the money rate should be equal to 'the' natural rate... Dr. Hayek now acknowledges the multiplicity of the 'natural' rates, but he has nothing more to say on this specific point than that they 'all would be equilibrium rates'. The only meaning (if it be a meaning) I can attach to this is that his maxim of policy now requires that the money rate should be equal to all these divergent natural rates."-- Piero Sraffa (1932b)So what does this victory of Sraffa over Hayek amount to? It's very puzzling, and you won't find any help here. This defeat for Austrian business cycle theory puzzled contemporaries too:

"I wish [Hayek] or someone would try to tell me in a plain grammatical sentence what the controversy between Sraffa and Hayek is about. I haven't been able to find anyone on this side who has the least idea." - Frank Knight to Oscar Morgenstern (as quoted by Caldwell)Update: Some additional quotations for commentators' amusement:

"The starting-point and the object of Dr. Hayek's inquiry is what he calls 'neutral money'; that is to say, a kind of money which leaves production and the relative price of goods, including the rate of interest, 'undisturbed', exactly as they would be if there were no money at all...References

...But the reader soon realizes that Dr. Hayek completely forgets to deal with the task which he has set himself... Being entirely unaware that it may be doubted whether under a system of barter the decisions of individuals would have their full effects, once he has satisfied himself that a policy of constant money would achieve this result, he identifies it with 'neutral money'; and finally, feeling entitled to describe that policy as 'natural', he takes it for granted that it will be found desirable by every right-thinking person. So that 'neutral' money ... in the end becomes 'our maxim of policy'.

If Dr. Hayek had adhered to his original intention, he would have seen at once that the differences between a monetary and a non-monetary economy can only be found in those characteristics which are set forth at the beginning of every textbook on money. That is to say, that money is not only the medium of exchange, but also a store of value, and the standard in terms of which debts, and other legal obligations, habits, opinions, conventions, in short all kinds of relations between men, are more or less rigidly fixed. As a result, when the price of one or more of these commodities changes, these relations change in terms of such commodities; while if they had been fixed in commodities, in some specified way, they would have changed differently, or not at all..

It would be idle to rehearse these platitudes had not Dr. Hayek completely ignored them... The money which he contemplates is ... used purely and simply as a medium of exchange. There are no debts, no money-contracts, no wage-agreements, no sticky prices in his suppositions..." -- Piero Sraffa (1932a)

- Hayek, F. A. (1932). "Money and Capital: A Reply", Economic Journal (reprinted in Hayek 1995), V. 42 (June): 237-249

- Hayek, F. A. (1995). The Collected Works of F. A. Hayek: Volume 9: Contra Keynes and Cambridge: Essays, Correspondence (edited by Bruce Caldwell), University of Chicago Press

- Sraffa, Piero (1932a). "Dr. Hayek on Money and Capital", Economic Journal (reprinted in Hayek 1995), V. 42 (March): 42-53.

- Sraffa, Piero (1932b). "A Rejoinder", Economic Journal (reprinted in Hayek 1995), V. 42 (June): 249-251

Friday, February 16, 2007

Andrew Kliman's Latest

I have just started reading Andrew Kliman's new book, Reclaiming Marx's "Capital": A Refutation of the Myth of Inconsistency. I haven't read the earlier The New Value Controversy and the Foundations of Economics, but I have read the even earlier Marx and Non-Equilibrium Economics and numerous journal and conference papers. The literature on the Temporal Single System Interpretation (TSSI) is large. Some of it consists of criticism by Sraffians. The New Interpretation (NI) of Gérard Duménil and Duncan Foley is also at play in recent literature on Marx's transformation problem. And some contributions have been made by scholars who might not self-identify with the interpretations put forward by any of these three schools.

I think I might have first read Alan Freeman in his contribution to Ricardo, Marx, Sraffa. I know I did not appreciate that essay as a developed interpretation of Marx's mathematical economics. It is only with later works that I saw something in the TSSI to agree or disagree with.

And generally I do disagree. I think both Freeman and Kliman write clear and amusingly, unlike the Hegelese some of their colleagues sometimes use. I can see how Marx was interpreted as consistent in his analysis of the transformation problem, even prior to the development of the TSSI. Unlike Kliman's claims for the TSSI, Eatwell's Sraffian interpretation does not maintain the law of the falling rate of profit. I thought Kliman was just wrong in his claim to refute the Okishio theorem, but I see that he has not conceded a mistake.

I did think about taking a pass on Kliman's book, since I think I may be familiar with the argument. I am interested in what textual evidence he put forwards for the TSSI interpretation. I suspect he will not address the question of whether Ricardo had a dual system. Marx criticizes confusion in Ricardo and other classical economists. Some of these criticisms are well taken; Ricardo doesn't always clearly distinguish between labor values and natural prices. Can one read those criticisms as putting forward the TSSI as the proper way to relate values and prices? It will not surprise me if Kliman does not address this question. (I don't think this question has been formulated in this way in the literature.)

I append a bibliography of some criticisms of the TSSI. I don't recall the substance of most of these criticisms. I gather that advocates of the TSSI have responded to most of these articles.

Maybe I'll write more when I get further along in Kliman's book.

I think I might have first read Alan Freeman in his contribution to Ricardo, Marx, Sraffa. I know I did not appreciate that essay as a developed interpretation of Marx's mathematical economics. It is only with later works that I saw something in the TSSI to agree or disagree with.

And generally I do disagree. I think both Freeman and Kliman write clear and amusingly, unlike the Hegelese some of their colleagues sometimes use. I can see how Marx was interpreted as consistent in his analysis of the transformation problem, even prior to the development of the TSSI. Unlike Kliman's claims for the TSSI, Eatwell's Sraffian interpretation does not maintain the law of the falling rate of profit. I thought Kliman was just wrong in his claim to refute the Okishio theorem, but I see that he has not conceded a mistake.

I did think about taking a pass on Kliman's book, since I think I may be familiar with the argument. I am interested in what textual evidence he put forwards for the TSSI interpretation. I suspect he will not address the question of whether Ricardo had a dual system. Marx criticizes confusion in Ricardo and other classical economists. Some of these criticisms are well taken; Ricardo doesn't always clearly distinguish between labor values and natural prices. Can one read those criticisms as putting forward the TSSI as the proper way to relate values and prices? It will not surprise me if Kliman does not address this question. (I don't think this question has been formulated in this way in the literature.)

I append a bibliography of some criticisms of the TSSI. I don't recall the substance of most of these criticisms. I gather that advocates of the TSSI have responded to most of these articles.

Maybe I'll write more when I get further along in Kliman's book.

- Laibman, David (2000). "Rhetoric and Substance in Value Theory: An Appraisal of the New Orthodox Marxism", Science & Society, V. 64, N. 3 (Fall): 310-332

- Mohun, Simon (2003). "On the TSSI and the Exploitation Theory of Profit", Capital and Class (Autumn): 85-102

- Mongiovi, Gary (2002). "Vulgar Economy in Marxian Garb: A Critique of Temporal Single System Marxism", Review of Radical Political Economics, V. 34: 393-416

- Screpanti, Ernesto (2005). "Guglielmo Carchedi's 'Art of Fudging' Explained to the People", Review of Political Economy, V. 17, N. 1 (January): 115-126

- Veneziani, Roberto (2004). "The Temporal Single-System Interpretation of Marx's Economics: A Critical Evaluation", Metroeconomica, V. 55, N. 1: 96-114

- Veneziani, Roberto (2005). "Dynamics, Disequilibrium, and Marxian Economics: A Formal Analysis of Temporal Single-System Marxism", Review of Radical Political Economics, V. 37, N. 4 (Fall): 517-529

Thursday, February 15, 2007

The Scepticism That I Advocate

"The scepticism that I advocate amounts only to this[:] That when the experts are agreed , the opposite opinion cannot held to be certain..." -- Bertrand RussellSadly the president of the Czech Republic is quite confused. He says, "each serious person and scientist" says that global warming is a myth. Contrast with Philip Ball, a science journalist.

Duke Economists On Certain Lacrosse Players

Last month, Roy Weintraub was the first signature on an open letter proclaiming Duke faculty to be welcoming to all students, including lacrosse players.

My take is that Syracuse lacrosse hasn't been that excellent the last two years, since Michael Powell graduated. Even if Syracuse is back on track this year, I don't have a position on whether the local team benefits or not if Duke is banned from the NCAAs, which I assume they will not be this year.

More seriously, I don't have much of an opinion on the rape charges, though I am aware of some of the troublesome stories about alleged prosecutorial misconduct. But I do have a high opinion of Weintraub and find interesting the work of certain Duke economists. Weintraub often writes about historiography and, from the little I know, seems interested in promoting the health of academic communities. I think this letter is an attempt to promote such healing.

My take is that Syracuse lacrosse hasn't been that excellent the last two years, since Michael Powell graduated. Even if Syracuse is back on track this year, I don't have a position on whether the local team benefits or not if Duke is banned from the NCAAs, which I assume they will not be this year.

More seriously, I don't have much of an opinion on the rape charges, though I am aware of some of the troublesome stories about alleged prosecutorial misconduct. But I do have a high opinion of Weintraub and find interesting the work of certain Duke economists. Weintraub often writes about historiography and, from the little I know, seems interested in promoting the health of academic communities. I think this letter is an attempt to promote such healing.

Tuesday, February 13, 2007

I Don't Care to Belong to a Club That Accepts People Like Me as Members

For some reason, some of the bloggers on my blogroll have simultaneously decided to talk about Marx:

- For once, I don't strongly object to Brad DeLong's take (other for than the emotional hostility directed towards Foley)

- I read Theories of Surplus Value before I read the first volume of Capital

- DSquared also has a go. Elsewhere he recommends a book I wonder if I should purchase.

Mainstream Economics Marred By False Consciousness?

"In 1966, if not 1985, a reasonable person not prone to excessive optimism would have expected the state of economics to be better in 2000 than it turned out to be; that is to say, with the mainstream less in thrall to marginalism than previously, not more acquiescent. The actual outcome is definitely a failure of some kind... is it always to be that an intellectual discipline so intimately involved with material interests will be marred by false consciousness? One might point to Ricardo as evidence for the possibility of non-mystifying economics. Or was a David Ricardo only possible in a time before economic analysis became an institutionalized element of the structure of social goverance?" -- Tony Aspromourgos, "Sraffian Research Programmes and Unorthodox Economics", Review of Political Economy, April 2004As I understand it, Tony Aspromourgos recently gave a presentation at a conference on Social Structures of Accumulation. (It will be a long while before I have read these proceedings.)

Monday, February 12, 2007

Bifurcations and "Perverse" Switch Points

1.0 Introduction

I seem to be slow in writing up these results into a working paper. So I thought I would just present them here.

The model in this post is an example of reswitching. The model is closed in a neoclassical framework, that is with an overlapping generations, representative agent approach. Nevertheless, two closures are presented. The details of the utility functions differ between the closures.

The variations of stationary states with utility function parameters are explored. This is an analysis of structural stability, in some sense. Multiple equilibria arise for some ranges of parameter values. But whether multiple equilibria are associated with the "normal" or the "perverse" switch varies between the two examples.

I think these results may be a challenge to Rosser's (1983) identification of reswitching with a cusp catastrophe. (I don't fully understand catastrophe theory. My favorite bifurcations are Hopf bifurcations and period-doubling, although even the chaotic mathematics of, say, the Lorenz equations is a stretch for me.) I think these results could be used to more strongly contrast with Rosser's if I considered two parameters in the first closure. The second parameter could be, for example, related to a coefficient of production.

This sensitivity to modeling details, of which switch point is associated with multiple equilibria, may also have implications for some sort of dynamic stability analysis. These results suggest that perhaps "perverse" switches are not necessarily associated with dynamic instability. A fuller analysis might lead me to come down disappointingly on Mandler's (2005) side in his debate with Garegnani and Schefold. (I'm uncomfortable with the emphasis in that debate being on tâtonnement stability, to the exclusion of the analysis of paths in models of temporary equilibria.)

2.0 First Closure

In this model, a single agent is born at the start of each each. The agents in each generation have identical utility functions, and they live for two years. In this closure, the agent is a worker for the first year of his life and retired in the second (Figure 1). He is paid wages at the end of his first year for the year of labor services he sells during that year. Out of those wages, he purchases some corn to consume immediately. The remainder he saves at the prevailing interest rate in the second year, for consumption of corn at the end of the last year of his life. The intertemporal consumption decision is modeled as a constrained maximization of a Cobb-Douglas utility function.

The utility function in this closure contains a single parameter. A higher value of this parameter is associated with agents less likely to defer consumption. Outdated neoclassical intuition would lead one to expect a higher value of this parameter to be associated with a smaller supply of "capital" and a corresponding higher stationary state interest rate. But the relation in this model between the stationary state interest rate and this parameter (Figure 2) is not non-decreasing.

3.0 Second Closure

This closure differs from the first in that the agent chooses how much labor to supply each of the two years of his life. That is, the agent's utility-maximization problem embodies a trade-off between leisure and goods in each year, as well as intertemporal trade-offs. The utility function is of a different form than in the first closure. Two parameters of the utility function control the agent's decisions.

Accordingly stationary state values of endogenous values (for example, the interest rate) form a two-dimensional manifold in a three-dimensional space. Figure 3 shows a slice through such a manifold in which one parameter of the utility function is kept constant. A higher value of the varying parameter is associated with a lesser willingness to defer consumption, that is, a smaller supply of "capital", in some sense. One trained with outdated neoclassical intuition would expect the relation graphed in Figure 3 to be non-decreasing. That is, one so mistrained would expect a smaller supply of capital to be associated with a larger stationary-state interest rate. But here too the relation shown is sometimes decreasing.

Figure 4 shows another slice through a manifold. In this case, the parameter controlling the relative desirability of consumption goods and leisure in each year varies, while the other parameter of the utility function is kept constant. A higher value of the varying utility function parameter is associated with a smaller willingness to supply labor. Given outdated neoclassical intuition, one would expect the relation graph to be non-decreasing. Here too the relation shown demonstrates such intuition to be mistaken.

References

I seem to be slow in writing up these results into a working paper. So I thought I would just present them here.

The model in this post is an example of reswitching. The model is closed in a neoclassical framework, that is with an overlapping generations, representative agent approach. Nevertheless, two closures are presented. The details of the utility functions differ between the closures.

The variations of stationary states with utility function parameters are explored. This is an analysis of structural stability, in some sense. Multiple equilibria arise for some ranges of parameter values. But whether multiple equilibria are associated with the "normal" or the "perverse" switch varies between the two examples.

I think these results may be a challenge to Rosser's (1983) identification of reswitching with a cusp catastrophe. (I don't fully understand catastrophe theory. My favorite bifurcations are Hopf bifurcations and period-doubling, although even the chaotic mathematics of, say, the Lorenz equations is a stretch for me.) I think these results could be used to more strongly contrast with Rosser's if I considered two parameters in the first closure. The second parameter could be, for example, related to a coefficient of production.

This sensitivity to modeling details, of which switch point is associated with multiple equilibria, may also have implications for some sort of dynamic stability analysis. These results suggest that perhaps "perverse" switches are not necessarily associated with dynamic instability. A fuller analysis might lead me to come down disappointingly on Mandler's (2005) side in his debate with Garegnani and Schefold. (I'm uncomfortable with the emphasis in that debate being on tâtonnement stability, to the exclusion of the analysis of paths in models of temporary equilibria.)

2.0 First Closure

In this model, a single agent is born at the start of each each. The agents in each generation have identical utility functions, and they live for two years. In this closure, the agent is a worker for the first year of his life and retired in the second (Figure 1). He is paid wages at the end of his first year for the year of labor services he sells during that year. Out of those wages, he purchases some corn to consume immediately. The remainder he saves at the prevailing interest rate in the second year, for consumption of corn at the end of the last year of his life. The intertemporal consumption decision is modeled as a constrained maximization of a Cobb-Douglas utility function.

|

| Figure 1: Overlapping Generations |

|

| Figure 2: Equilibrium Interest Rates in First Closure |

3.0 Second Closure

This closure differs from the first in that the agent chooses how much labor to supply each of the two years of his life. That is, the agent's utility-maximization problem embodies a trade-off between leisure and goods in each year, as well as intertemporal trade-offs. The utility function is of a different form than in the first closure. Two parameters of the utility function control the agent's decisions.

Accordingly stationary state values of endogenous values (for example, the interest rate) form a two-dimensional manifold in a three-dimensional space. Figure 3 shows a slice through such a manifold in which one parameter of the utility function is kept constant. A higher value of the varying parameter is associated with a lesser willingness to defer consumption, that is, a smaller supply of "capital", in some sense. One trained with outdated neoclassical intuition would expect the relation graphed in Figure 3 to be non-decreasing. That is, one so mistrained would expect a smaller supply of capital to be associated with a larger stationary-state interest rate. But here too the relation shown is sometimes decreasing.

|

| Figure 3: Equilibrium Interest Rates in Second Closure |

|

| Figure 4: Equilibrium Wages in Second Closure |

References

- Garegnani, P. (2005a). "Capital and Intertemporal Equilibria: A Reply to Mandler", Metroeconomica, V. 56, Iss. 4 (Nov): 411-437.

- Garegnani, P. (2005b). "Further on Capital and Intertemporal Equilibria: A Rejoinder to Mandler", Metroeconomica, V. 56, Iss. 4 (Nov): 495-502.

- Mandler, Michael (2005). "Well-Behaved Production Economies", Metroeconomica, V. 56, Iss. 4 (Nov): 477-494.

- Parrinello, Sergio (2005). "Intertemporal Competitive Equilibrium, Capital and the Stability of Tatonnement Pricing Revisited", Metroeconomica, V. 56, Iss. 4 (Nov): 514-531.

- Rosser, J. B., Jr. (1983). "Reswitching as a Cusp Catastrophe", Journal of Economic Theory, V. 31, N. 1: 182-193.

- Schefold, B. (2005a). "Reswitching as a Cause of Instability of Intertemporal Equilibrium", Metroeconomica, V. 56, Iss. 4 (Nov): 438-476.

- Schefold, B. (2005b). "Zero Wages - No Problem? A Reply to Mandler", Metroeconomica, V. 56, Iss. 4 (Nov): 503-513.

Saturday, February 10, 2007

Wittgenstein and Marxism

Ralph Dumain has compiled a bibliography on Wittgenstein, Marxism, and Sociology. It contains, for example, the Moran article in the New Left Review that I had previously noted, but neither the Eagleton nor the Robinson article in my list. But it does contain lots more to read.

Wednesday, February 07, 2007

A Revolutionary Encylopedia

I find this post, about this joke of interest.

But in my post title, I refer to Diderot's Encylopedia. To see human knowledge set out in a structured form that anybody can read is to see a revolution in the making. No longer must one depend on the authority of the nobility and priests for interpretation and direction of one's beliefs.

Some economists might find the entries on "Corn" and "Farmers" in the Encyclopedia of interest. As I understand it, François Quesnay wrote these. These entries, at least in the original French, are available online.

I'm not a registered Wikipedia user. And I've edited articles over a number of years from a number of computers where my IP is randomized. So I've long lost track of what I've contributed. I thought I wrote something about Francois Quesnay, but I can find no traces in the current entry. I also see a definite error. Maybe I wrote something about physiocracy, but here, too, my words have vanished. (On the other hand, the entry on Post Keynesianism retains some of what I wrote, while being much improved (chiefly by Jim Devine).)

Some think Piero Sraffa was influenced in his "corn model" interpretation of David Ricardo by Karl Marx's Theories of Surplus Value interpretation of Quesnay.

But in my post title, I refer to Diderot's Encylopedia. To see human knowledge set out in a structured form that anybody can read is to see a revolution in the making. No longer must one depend on the authority of the nobility and priests for interpretation and direction of one's beliefs.

Some economists might find the entries on "Corn" and "Farmers" in the Encyclopedia of interest. As I understand it, François Quesnay wrote these. These entries, at least in the original French, are available online.

I'm not a registered Wikipedia user. And I've edited articles over a number of years from a number of computers where my IP is randomized. So I've long lost track of what I've contributed. I thought I wrote something about Francois Quesnay, but I can find no traces in the current entry. I also see a definite error. Maybe I wrote something about physiocracy, but here, too, my words have vanished. (On the other hand, the entry on Post Keynesianism retains some of what I wrote, while being much improved (chiefly by Jim Devine).)

Some think Piero Sraffa was influenced in his "corn model" interpretation of David Ricardo by Karl Marx's Theories of Surplus Value interpretation of Quesnay.

Example With Heterogeneous Labor (Part 3 of 3)

4.0 Prices

The argument proceeds by determining which technique is cost minimizing when the firms in all industries are in equilibrium. In this context, a full industry equilibrium has the following properties:

(Notice the above conditions are not enough to specify a general equilibrium. Utility maximization, the supply of originary factors, and the demand for consumption goods, for example, are not modeled.)

Given the above conditions, Equations 1 and 2 must be satisfied if the Alpha technique is adopted by the firms:

Corresponding solutions for the systems of equations arising for the Beta, Gamma, and Delta techniques are relegated to Appendix C.

5.0 Choice of Technique

The system of equations described in Section 4 for a given technique guarantee that costs, including interest charges, do not exceed revenues for the processes comprising that technique. They also guarantee that no pure economic profits can be earned by operating either one of those processes. They do not guarantee that no pure economic profits can be earned in the processes outside that technique. That is, it remains to be shown which technique is cost-minimizing. The so-called factor-price frontier can be used to analyze the choice of technique.

For this example, the factor-price frontier is a two-dimensional surface in a three-dimensional space. The dimensions of that space are the rate of profits and the wages for the two categories of labor. I consider a slice through the frontier for two separate values of the rates of profits.

5.1 A Rate of Profits of 0%

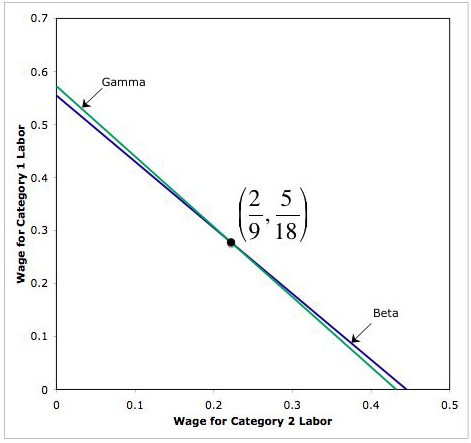

Figure 2 shows the factor-price curves for three techniques when the rate of profits is zero. (The curve for the Delta technique is never on the frontier formed from the outer envelope of these curves, and it is not shown.) The cost-minimizing technique at a given rate of profits and a given wage of category 2 labor maximizes the wage of category 1 labor. Thus, for a rate of profits of zero percent, the Alpha technique is cost minimizing at a low wage of category 2 labor, the Beta technique is cost-minimizing at an intermediate wage, and the Gamma technique is cost-minimizing at a high wage. (Notice that the curves for the techniques are straight lines in the figure. This is a general implication of the mathematics. Reswitching of techniques cannot arise at a given level of the rate of profits for varying levels of the wages of the two categories of labor.)

Since the technique and prices have been determined at a zero percent rate of profits, for any given wage of category 2 labor, one can graph the labor intensity for category 2 labor for the cost-minimizing technique against the wage of category 2 labor. Figure 3 shows the result. In this case, a higher wage of category 2 labor is associated with a step-decrease in the labor intensity of category 2 labor. For this specific example, the behavior at an interest rate of zero percent seems to conform to ill-educated and outdated neoclassical intuition about factor substitution.

5.2 A Rate of Profits of 150%

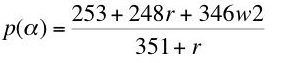

Figure 4 shows the factor-price curves on the frontier when the rate of profits is 150 percent. In this case, the Gamma technique is cost-minimizing at a low wage of category 2 labor, while the Beta technique is cost-minimizing at a high wage.

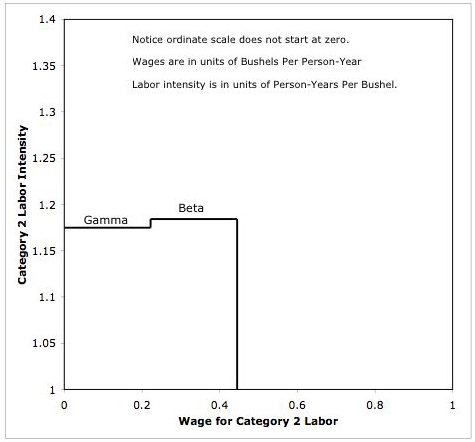

Figure 5 shows the labor-intensity of category 2 labor graphed against the wage of category 2 labor. In this case, a higher wage is associated with a choice of technique in which a more labor intensive technique. It is mathematically incorrect to state that, given typical neoclassical assumptions, firms will substitute another category of labor if the wage of one category of labor is increased.

6.0 Conclusion

So much for explaining wages and employment by the interaction of well-behaved supply and demand functions for labor categories in any practical application, as such functions are understood in neoclassical economics.

(A counterargument would show how to draw empirically-applicable, downward-sloping labor demand functions in this and related examples; point out some typical neoclassical assumption violated in this and related examples; state empirically validated special-case conditions on, say, technology that rule out these sort of Sraffa effects; show how the rejection of the old-fashioned neoclassical story about substitution effects is consistent with typical applications; or, perhaps, reject such applications.)

Appendix C

Appendix C.1 Beta Prices

Appendix C.3 Delta Prices

References

The argument proceeds by determining which technique is cost minimizing when the firms in all industries are in equilibrium. In this context, a full industry equilibrium has the following properties:

- At least one corn-producing process is operated, and at least one steel-producing process is operated

- The cost of inputs, including interest charges, for each process in operation does not exceed revenues

- No process can be used to obtain pure economic profits

(Notice the above conditions are not enough to specify a general equilibrium. Utility maximization, the supply of originary factors, and the demand for consumption goods, for example, are not modeled.)

Given the above conditions, Equations 1 and 2 must be satisfied if the Alpha technique is adopted by the firms:

(1)

where corn is the numeraire, p is the price of steel, w1 is the wage of category 1 labor, w2 is the wage of category 2 labor, and r is the rate of profits (sometimes called the interest rate). The constants in Equation 1 come from the steel-producing process (Process A) in the alpha technique. The constants in Equation 2 come from the corn-producing process (Process D). Equations 1 and 2 provide a system of two equations in four unknowns. Thus, two degrees of freedom exist in this system. The system can be solved for the wage of category 1 labor and the price of steel in terms of a given rate of profits and a given wage of category 2 labor.(2)

(3)

Equation 3 is the so-called factor price surface for the Alpha technique. This is a two-dimensional surface in a three-dimensional space.(4)

Corresponding solutions for the systems of equations arising for the Beta, Gamma, and Delta techniques are relegated to Appendix C.

5.0 Choice of Technique

The system of equations described in Section 4 for a given technique guarantee that costs, including interest charges, do not exceed revenues for the processes comprising that technique. They also guarantee that no pure economic profits can be earned by operating either one of those processes. They do not guarantee that no pure economic profits can be earned in the processes outside that technique. That is, it remains to be shown which technique is cost-minimizing. The so-called factor-price frontier can be used to analyze the choice of technique.

For this example, the factor-price frontier is a two-dimensional surface in a three-dimensional space. The dimensions of that space are the rate of profits and the wages for the two categories of labor. I consider a slice through the frontier for two separate values of the rates of profits.

5.1 A Rate of Profits of 0%

Figure 2 shows the factor-price curves for three techniques when the rate of profits is zero. (The curve for the Delta technique is never on the frontier formed from the outer envelope of these curves, and it is not shown.) The cost-minimizing technique at a given rate of profits and a given wage of category 2 labor maximizes the wage of category 1 labor. Thus, for a rate of profits of zero percent, the Alpha technique is cost minimizing at a low wage of category 2 labor, the Beta technique is cost-minimizing at an intermediate wage, and the Gamma technique is cost-minimizing at a high wage. (Notice that the curves for the techniques are straight lines in the figure. This is a general implication of the mathematics. Reswitching of techniques cannot arise at a given level of the rate of profits for varying levels of the wages of the two categories of labor.)

|

| Figure 2: Factor Price Fronter At r = 0% |

|

| Figure 3: Category 2 Labor Intensity Versus Wage At r = 0% |

5.2 A Rate of Profits of 150%

Figure 4 shows the factor-price curves on the frontier when the rate of profits is 150 percent. In this case, the Gamma technique is cost-minimizing at a low wage of category 2 labor, while the Beta technique is cost-minimizing at a high wage.

|

| Figure 4: Factor Price Fronter At r = 150% |

|

| Figure 5: Category 2 Labor Intensity Versus Wage At r = 150% |

6.0 Conclusion

So much for explaining wages and employment by the interaction of well-behaved supply and demand functions for labor categories in any practical application, as such functions are understood in neoclassical economics.

(A counterargument would show how to draw empirically-applicable, downward-sloping labor demand functions in this and related examples; point out some typical neoclassical assumption violated in this and related examples; state empirically validated special-case conditions on, say, technology that rule out these sort of Sraffa effects; show how the rejection of the old-fashioned neoclassical story about substitution effects is consistent with typical applications; or, perhaps, reject such applications.)

Appendix C

Appendix C.1 Beta Prices

(C-1)

Appendix C.2 Gamma Prices(C-2)

(C-3)

(C-4)

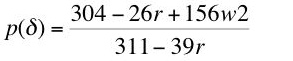

Appendix C.3 Delta Prices

(C-5)

(C-6)

References

- Kurz, Heinz D. and Neri Salvadori (1995). Theory of Production: A Long-Period Analysis, Cambridge University Press

- Metcalfe, J. S. and Ian Steedman (1972). "Reswitching and Primary Input Use", Economic Journal

Monday, February 05, 2007

Example With Heterogeneous Labor (Part 2 of 3)

3.0 Quantity Flows

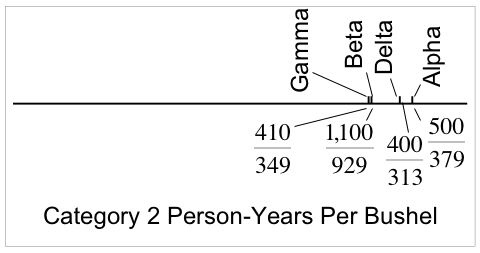

The example is constructed by comparing constant prices associated with stationary states for producing the net output of a bushel corn. Four stationary states are possible, or linear combinations of them. Each of the four pure stationary states corresponds to a choice of one of the techniques. Table 4 shows the quantity flows for a stationary state in which the alpha technique is used. The quantity flows for the stationary states in which the other techniques are used are shown in Appendix B.

Notice that the steel used up as an input in the stationary state shown in Table 4 is exactly replaced by the output of the steel industry. After replacing the corn used up as inputs in the two industries, the net output of this stationary state is one bushel corn. And (500/379) person-years of category 2 labor are used to produce this net output. Thus, for the alpha technique, the category 2 labor intensity of corn output is (500/379) person-years per bushel, as shown in Figure 1. The category 2 labor intensities for the other techniques can easily be calculated from the Tables in the appendix.

Appendix B

The example is constructed by comparing constant prices associated with stationary states for producing the net output of a bushel corn. Four stationary states are possible, or linear combinations of them. Each of the four pure stationary states corresponds to a choice of one of the techniques. Table 4 shows the quantity flows for a stationary state in which the alpha technique is used. The quantity flows for the stationary states in which the other techniques are used are shown in Appendix B.

| Inputs | Steel Industry | Corn Industry |

| Category 1 Labor | (1/379) Person-Year | (350/379) Person-Year |

| Category 2 Labor | (100/379) Person-Years | (400/379) Person-Years |

| Steel | 0 Ton | (100/379) Ton |

| Corn | (71/379) Bushel | (50/379) Bushel |

| Outputs | (100/379) Tons Steel | (500/379) Bushels Corn |

|

| Figure 1: Technique By Category 2 Labor Intensity |

| Inputs | Steel Industry | Corn Industry |

| Category 1 Labor | (1/929) Person-Year | (1,000/929) Person-Years |

| Category 2 Labor | (100/929) Person-Year | (1,000/929) Person-Years |

| Steel | 0 Ton | (100/929) Ton |

| Corn | (71/929) Bushel | 0 Bushel |

| Outputs | (100/929) Tons Steel | (1,000/929) Bushels Corn |

| Inputs | Steel Industry | Corn Industry |

| Category 1 Labor | (33/349) Person-Year | (350/349) Person-Years |

| Category 2 Labor | (60/349) Person-Year | (350/349) Person-Years |

| Steel | (15/349) Ton | (35/349) Ton |

| Corn | (1/349) Bushel | 0 Bushel |

| Outputs | (50/349) Tons Steel | (350/349) Bushels Corn |

| Inputs | Steel Industry | Corn Industry |

| Category 1 Labor | (66/313) Person-Years | (245/313) Person-Years |

| Category 2 Labor | (120/313) Person-Years | (280/313) Person-Years |

| Steel | (30/313) Ton | (70/313) Tons |

| Corn | (2/313) Bushel | (35/313) Bushel |

| Outputs | (100/313) Tons Steel | (350/313) Bushels Corn |

Sunday, February 04, 2007

Example With Heterogeneous Labor (Part 1 of 3)

1.0 Introduction

I thought I would go through another example in which firms want to hire more workers (per unit output) at a higher wage. Since the last time I presented such an example, I've learned more about how to present mathematics in a blog post.

This example was originally developed by Metcalfe and Steedman. I've renamed the inputs so as to present it as a case of non-competing types of heterogeneous labor. I don't think reswitching need occur for the behavior illustrated in Figure 5 in the third part to occur.

2.0 Data On Technology

Consider a very simple economy that produces a single consumption good, corn, from inputs of two categories of labor, steel, and (seed) corn. All production processes in this example require a year to complete. Two production processes are known for producing steel. These processes require the inputs shown in Table 1 to be available at the start of the year for each ton steel produced and available at the end of the year. Two processes, as shown in Table 2, are also known for producing corn.

A technique consists of a process for producing the consumption good, corn, and a process for producing each non-consumption reproducible good used as an input in the process for producing the consumption good. In other words, a technique is a combination of one steel-producing process and one corn-producing process. The number of techniques is the product of the number of corn-producing processes and the number of steel-producing process. Thus, four techniques exist in this example. They are defined in Table 3.

Appendix A

The production functions that describe the technology in this example exhibit common neoclassical features: Constant Returns to Scale and non-increasing marginal returns to each factor. For purposes of constructing the production function for corn, the quantities of both categories of labor, steel, and corn available as input to corn production are taken as given. Let Q01, Q02, Q1, and Q2 be these quantities of category one labor, category two labor, steel, and corn, respectively. All quantities are measured in physical units (person-years, tons, bushels). The following Linear Program expresses the problem of maximizing the output of corn from these inputs: choose X1 and X2, the quantities of corn produced by processes C and D, respectively, to maximize:

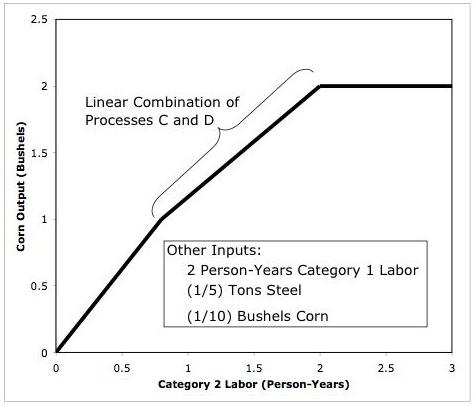

One standard method of visualizing production functions is with isoquants. An isoquant for this production function is a four dimensional surface, which I find difficult to draw. Accordingly, suppose the inputs of category 1 labor and corn are not binding for the level of output for which isoquants are drawn. Then Figure A-1 shows the isoquants for the corn production function in the remaining two dimensions. The dashed rays from the origin correspond to the two processes available for producing corn. If only one process for producing corn was known (a Leontief production function or "fixed coefficients" of production), an isoquant would consist of two rays, one extending horizontally right from the dashed line and the other extending vertically upward from the dashed line for that process. For the two known processes, an isoquant also contains the line segment shown sloping downward to the right. This line segment corresponds to a linear combination of the processes C and D, in which coefficients of production continuously vary.

One can also consider the (physical) marginal product of category 2 labor as the slope of the function shown in Figure A-2. In this case, no inputs except category 2 labor are binding for the lowest quantities of category 2 labor input. Since process D produces more corn than process C per person-year of category 2 labor, process D provides the steepest part of this projection of the production function for corn. When the steel input becomes binding, the marginal product of category 2 labor declines to the slope of the line segment corresponding to linear combinations of the two processes. Finally, the other inputs constrain a corn-producing firm to only adopt process C for a fixed level of output, and the marginal product of category 2 labor is zero. For this model of technology the marginal product of each input is a decreasing step function.

A textbook presentation of production functions to students assumed to know the calculus often presents smooth isoquants and production functions that are at least twice continuously differentiable. A discrete model of technology can approximate smooth functions arbitrarily closely, given enough processes. When more processes are available, more line segments representing linear combinations of processes arise. Smooth production functions correspond to the limit, in which there an uncountably infinite number of processes available. As I understand it, no point in the limit case, however, corresponds to a linear combination of processes. "Perverse" Sraffa effects can arise in both a discrete and a smooth technology. But I like Linear Programming, and will stick to a discrete model of technology.

I thought I would go through another example in which firms want to hire more workers (per unit output) at a higher wage. Since the last time I presented such an example, I've learned more about how to present mathematics in a blog post.

This example was originally developed by Metcalfe and Steedman. I've renamed the inputs so as to present it as a case of non-competing types of heterogeneous labor. I don't think reswitching need occur for the behavior illustrated in Figure 5 in the third part to occur.

2.0 Data On Technology

Consider a very simple economy that produces a single consumption good, corn, from inputs of two categories of labor, steel, and (seed) corn. All production processes in this example require a year to complete. Two production processes are known for producing steel. These processes require the inputs shown in Table 1 to be available at the start of the year for each ton steel produced and available at the end of the year. Two processes, as shown in Table 2, are also known for producing corn.

| Process A | Process B | |

| Category 1 Labor | (1/100) Person-Year | (33/50) Person-Year |

| Category 2 Labor | 1 Person-Year | (6/5) Person-Year |

| Steel | 0 Ton | (3/10) Ton |

| Corn | (71/100) Bushel | (1/50) Bushel |

| Process C | Process D | |

| Category 1 Labor | 1 Person-Year | (7/10) Person-Year |

| Category 2 Labor | 1 Person-Year | (4/5) Person-Year |

| Steel | (1/10) Ton | (1/5) Ton |

| Corn | 0 Bushel | (1/10) Bushel |

| Technique | Processes |

| Alpha | A, D |

| Beta | A, C |

| Gamma | B, C |

| Delta | B, D |

Appendix A

The production functions that describe the technology in this example exhibit common neoclassical features: Constant Returns to Scale and non-increasing marginal returns to each factor. For purposes of constructing the production function for corn, the quantities of both categories of labor, steel, and corn available as input to corn production are taken as given. Let Q01, Q02, Q1, and Q2 be these quantities of category one labor, category two labor, steel, and corn, respectively. All quantities are measured in physical units (person-years, tons, bushels). The following Linear Program expresses the problem of maximizing the output of corn from these inputs: choose X1 and X2, the quantities of corn produced by processes C and D, respectively, to maximize:

such that(A-1)

(A-2)

(A-3)

(A-4)

(A-5)

The production function for corn, f( Q01, Q02, Q1, Q2 ) is the value of the objective function, X* for the solution of the above Linear Program, expressed as a function of the physical inputs into corn production. These parameters define the right-hand-side of the linear constraints in Displays A-2 through A-5. The left-hand-side of these constraints is defined by the parameters in Table 2.(A-6)

{kind=link}

One standard method of visualizing production functions is with isoquants. An isoquant for this production function is a four dimensional surface, which I find difficult to draw. Accordingly, suppose the inputs of category 1 labor and corn are not binding for the level of output for which isoquants are drawn. Then Figure A-1 shows the isoquants for the corn production function in the remaining two dimensions. The dashed rays from the origin correspond to the two processes available for producing corn. If only one process for producing corn was known (a Leontief production function or "fixed coefficients" of production), an isoquant would consist of two rays, one extending horizontally right from the dashed line and the other extending vertically upward from the dashed line for that process. For the two known processes, an isoquant also contains the line segment shown sloping downward to the right. This line segment corresponds to a linear combination of the processes C and D, in which coefficients of production continuously vary.

|

| Figure A-1: Isoquants For Corn Production Function |

|

| Figure A-2: Outputs As Category 2 Labor Varies |