|

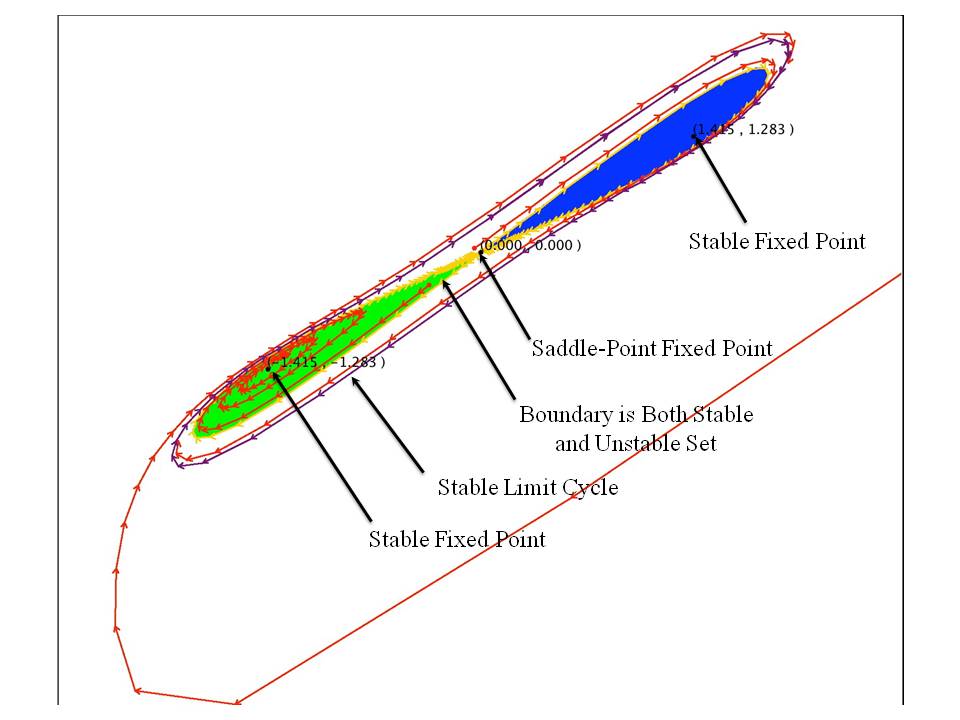

| Figure 1: A Fractal in the Phase Diagram for One Specification of Parameters in the Kaldor Model1 |

1.0 Introduction

I thought I would try to combine an ability for computers to draw

fractals

with an economic model that suggests practical conclusions. In this post, I

merely duplicate some results in the literature. In a deterministic

ergodic process, as I understand it, all trajectories pass through every state

in whatever attractor may exist. Hence, the Kaldor model, like

some

dynamical

systems arising in mathematics, is non-ergodic.

2.0 The Model

In 1940, Nicholas Kaldor proposed a model of the business cycle.

It can be expressed by four equations2.

National ouput evolves from the previous period as a response to

aggregate demand:

Yt+1 = Yt + α(It - St),

where

Yt is the value of output in year

t,

It is intended investment, and

St is intended saving.

The parameter

α represents the speed of adjustment to

excess aggregate demand. The evolution of the value of the capital

stock depends on investment and depreciation:

Kt+1 = It + (1 - δ)Kt,

where

δ is the depreciation rate of capital stock.

Intended saving is directly proportional to output:

St = σYt,

where

σ is the (average and marginal) propensity to save.

An investment function

3 is the final equation specifying the model:

It = σμ + γ(σμ/δ - Kt) + Tan-1(Yt - μ),

where

μ is the expected level of output, and

γ represents the costs of adjusting the capital stock.

Along with some restrictions on the values of parameters, the

model is now fully specified. The arc tangent function provides a

s-shaped non-linear term, such that entrepreneurs increase

investment when output exceeds their expectations

4.

I find it convenient to

define new variables normalized around a stationary state:

kt = Kt - σμ/δ

yt = Yt - μ

The model, expressed in terms of normalized capital stocks and normalized output, is:

kt + 1 = Tan-1(yt) + (1 - δ - γ)kt

yt + 1 = (1 - ασ)yt + αTan-1(yt) - αγkt

Note that the following is a solution:

For all time t,

yt = kt = 0.

3.0 Some Results

The above version of the Kaldor model is a discrete-time dynamical system, defined by a map from the two-dimensional real plane (k, y) to the same space. Four5 parameters are used to define the map. Questions for the mathematician revolve around describing how the phase portrait for the system varies qualitatively with variations in the parameters. Complex and chaotic behavior can arise in the Kaldor model with appropriate choices of parameter values.

For a small enough speed of adjustment and large enough propensity to save, the dynamics is boring. All trajectories converge to the origin.

As the propensity to save decreases, the system goes through a pitchfork bifurcation, so-called because the bifurcation diagram looks like a pitchfork. The origin loses its stability, and two symmetric fixed points appear. For a small enough speed of adjustment, at least, the two symmetric fixed points exhibit local asymptotic stability. The location of these new fixed points must be found numerically. A fortiori, the computer must be used as an aid to perform a local stability analysis of these points, based on the eigenvalues of the Jacobian matrix.

As the speed of adjustment increases, the boundary between the basins of attraction becomes more complex. Figure 1 shows a case where they are entangled in a fractal-like structure, and the outer perimeter of the colored area is repelling. The limit cycle shown is a short distance outside this repelling boundary.

I have by no means exhausted the dynamics of the Kaldor model. Consider a region in which the origin is the only fixed point, and it is asymptotically stable. As the speed of adjustment increases, the system undergoes a Neimark-Sacker bifurcation, which, I gather, is the discrete-time analog to a Hopf bifurcation. Cycles exist in which the cycle is not a fixed point on the Poincaré return map, but winds around many times before repeating. And if I want my application to explore all these dynamics, I have quite a bit of programming to do. I am curious if I will be able to plot a bifurcation diagram, given that the behavior at the limit depends on the initial value.

4.0 Observations

For the parameter values illustrated in the figures, trajectories have three possible destinations:

- A stable equilibrium with lots of capital and high output.

- Another stable equilibrium with less capital and less output.

- A business cycle.

Furthermore, the boundary between the basins of attraction for the stable

limit points is fractal-like. These properties suggest that a random shock

to the system can redirect trajectories to a very different final

destination.

Although not illustrated above, the model exhibits structural instability.

A perturbation of the model parameters can result in different observable

behavior, of greater or less complexity.

One general way of conceptualizing business cycles is to see them as the

response of a damped linear system to exogenous shocks. Their height

and depth depends on the characteristics of the external impulses driving

the system. The Kaldor model suggests another possibility. In this model,

the properties and extent of business cycles are endogenously determined.

Shocks can drive the system from one trajectory to another, but the

range of possible behaviors is determined from within the system. It is

my impression that the former way of understanding business cycles is

dominant among mainstream macroeconomists, while the latter is closer to

describing actually existing capitalist economies.

Footnotes

- Figure 1 is drawn with the parameter values specified in Figure 2(c) in Agliari et al (2007).

- Kaldor uses a nonlinear savings function and merely specifies the form of the investment function.

- The specification of investment independent of saving is an essential characteristic of Keynesian models.

- In this model, expectations are held constant.

- Notice the expected level of output does not appear in the two equations giving the normalized model.

Selected References

- A. Agliari, R. Dieci, and L. Gardini (2007). Homoclinic Tangles in a Kaldor-like Business Cycle Model. Journal of Economic Behavior & Organization. Vol. 62: 324-347.

- W. W. Chang and D. J. Smyth (1971). The Existence and Persistence of Cycles in a Non-linear Model: Kaldor's 1940 Model Rexamined. Review of Economic Studies. Vol. 38, No. 1: 37-44.

- Richard M. Goodwin (1951). The Nonlinear Accelerator and the Persistence of Business Cycles. Econometrica. Vol. 19, No. 1: 1-17.

- Nicholas Kaldor (1940). A Model of the Trade Cycle. Economic Journal. Vol. 50, No. 197: 78-92.

- Yuri A. Kuznetsov (1998). Elements of Applied Bifurcation Theory, 2nd edition.