Previously, I outlined a model on an economy in which wheat and corn are produced in yearly production cycles. If the profit-maximizing competitive firm produces wheat, it must solve the following mathematical programming problem:

Given w, P(1), P(2)

Choose a01, a11, a21 to

To Maximize(6)

Such that

The solution gives the following marginal productivity equations:

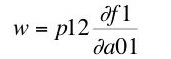

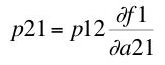

(7)

(8)

(9)

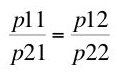

In competitive equilibrium, the price of every input is equal to the value of the marginal product for each product.

Pure economic profit must be nonnegative, for if it were negative the firm would have chosen not to produce at all. It works out that pure economic profit cannot be positive either. Equation 10 states that pure economic profit is zero in the wheat-producing industry:

(10)

An analogous set of three marginal productivity equations and a zero economic profit condition arises from analyzing corn-producing firms.

4.0 Interest Rates In Steady States

Consider the following definitions:

(11)

(12)

These are known as the own rates of interest of wheat and corn, respectively.

In a long run equilibrium, the quantities of wheat and corn inputs are not given. Assume they have been adjusted such that relative spot prices of corn, wheat, and labor remain unchanged from year to year. Almost all economists up until the late 1920s, as far as I am aware, thought of this constancy of relative prices, or an equivalent condition, as a defining property of long run equilibrium.

(It was about then that short-run notions of temporary and intertemporal equilibrium were introduced, and the economists' conceptions became more complex. Mistakes were made by the early neoclassicals. Walras thought he could take endowments of produced goods as given, but still consider an equilibrium with steady-state prices. Others mistakenly wanted to take the quantity of "capital" as given, but have its form, in terms of composition of wheat and corn, be endogenously determined.)

Certainly, we need to introduce some condition relating industries. Anyways, If you think about the condition of stationary spot prices, you will see that if no pure economic profits are possible, relative forward and relative spot prices must be equal:

(13)

Otherwise, an agent could buy or sell wheat or corn in the forward market for a year and make a pure economic profit on the spot market at the end of the year.

Therefore:

(14)

Or:

(15)

where r is the common own rate of interest for all commodities. It is not a parameter of some unobservable utility function, although it may become equal to some such parameter in equilibrium in special cases. Such a special case could be created by closing this model with utility-maximization by a infinitely-lived representative agent.

The condition of unchanging relative spot prices allows us to remove P(2) from our equations. We have:

(16)

The condition of no economic profit gives the following system of two equations:

(17)

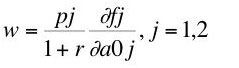

where I have dropped the time index on the price vector as being no longer needed. The marginal productivity equations become:

(18)

(19)

So we have a system of eight Equations - the two price equations (17), and the six marginal productivity equations (18) and (19). There are ten choice variables to be determined by the model:

- The wage w

- The common own rate of interest r

- Two prices, P = (p1, p2)

- Six production coefficients a0 and A

There is no equation equating r to some mystical, mythical, marginal product of capital.

In the next part, I outline the construction of the so-called factor price frontier.

8 comments:

Why, exactly, do you call intertemporal equilibrium "short-run equilibrium"?

If you want to say that models of intertemporal equilibrium are unrealistic, then that's something that can be discussed. But then, "long-run" equilibria are also unrealistic -- in the long run everything changes so it is rather foolish to say that the long-run equlibrium models are more realistic.

Secondly, although perhaps I should wait to see your "part 3" of this theme, given that you do not introduce any utility functions or in any other way characterize the influence of consumers on the economy, why should anyone take seriously any indeterminacy of the "profit rate" in your model?

What does your criticism bring to the table that is not contained in the phrase "since there is no such thing as aggregated 'capital' there is obviously no 'marginal product of capital'"?

The Arrow-Debreu model of intertemporal equilibium shold actually be referred to as "very short run". In the model, quantities of all capital goods, both fixed and variable are taken as given. Take a look at Fabio Petri's "General Equilibrium Theory and Professor Blaug"

My complaint is not one about "realism" of assumptions.

This series has four parts. In the fourth part I will verbally describe two nested models. I don't claim my point is highly original. It could be read as a explanation of certain comments in Duncan Foley's "Value, Distribution and Capital: A Review Essay" (Review of Political Economy, V. 13, N. 3, 2001).

I am quite aware that the model I describe is open. I do not object to "indeterminancy". Given the SMD results, though, I don't think one who rigorously understands the logic of neoclassical theory should argue that the particular neoclassical closure of this model explains regularities in the economy through utility maximization.

My criticism is not merely that aggregate 'capital' does not exist. It is attempt to get clear the logic of the disaggregated model. (Petri makes clear that many contemporary economists do not understand the role of an aggregate measure of capital in traditional neoclassical theory.)

Thanks for the reply.

Unfortunately, your link gives me a "FILE NON DISPONIBILE" error, and your comment that intertemporal equilibria should "actually be referred to as 'very short run'" is not very enlightening.

Yes, it is true that _initial_ quantities of all goods are taken as given, but then they are allowed to vary in time, as the equilibrium path unfolds. Goods --capital fixed or variable or simple goods -- are allowed to vary by being indexed by time. Taking the assumptions of the intertemporal equilibrium model as true, there is no obvious sense to the claim that the model is actually short-term.

One criticism of intertemporal equilibrium models (IEM) that actually makes sense, and can be interpreted as saying that the models are "short-term" is the following: as the equilibrium path unfolds, in the real world there will be small deviations from it. But these small deviations change the data needed for deriving the following equilibrium prices, so these small deviations imply the need to compute a different equilibrium path, thus making the initially determined equilibrium path irrelevant (and thus "short-term")

This is a valid criticism, but the (lack of) realism of the model enters crucially into the criticism by introducing deviations from the theoretically predicted path -- with no deviation (and the deviation is a concession to realism not to logic), the model is as long term as one wants it.

So I don't see how you can support your assertion that the "short-term" complaint is not one about the realism of assumptions. And as I've said, other "long-term" approaches can also be accused of lacking realism.

Regarding the indeterminacy question, what I'm getting at is that if you intend to criticize the (non-bastardized) neoclassical theory of distribution with this series of posts, then, to put it bluntly, your criticism is logically invalid.

This is so because by excluding utility maximization from the model you consider, the indeterminacy of wages/interest that follows is not an indeterminacy that is present in neoclassical models. There is no neoclassical claim that I'm aware of to the effect that one can determine distribution _without_ taking utility maximization into account.

Now, I'm perfectly aware that indeterminacies can arise in neoclassical models with utility maximization (as suggested by SMD and by some concrete examples) but the conditions and logic of those indeterminacies are quite different from the conditions of the one you use to illustrate your point.

Your series of posts can not then be taken as a logically valid criticism of the neoclassical theory of distribution, regardless of whether there are valid criticisms of it.

One could always use google to find Petri's working paper, number 486, in the series at Sienna. Maybe one of those links will work.

The rest of the above comments seem to me confused and irrelevant. I am quite aware that quantities vary over time in the Arrow-Debreu model of intertemporal equilibrium. (Perhaps I should have written "initial".) In fact, under some circumstances the proportions of quantities of capital goods approaches the long run ratios, those along the Von Neumann ray. (The Von Neumann ray has saddle-point (in)stability.) The turnpike theorem relates the very short-run A-D model to the long run Von Neumann model. In the latter model, the initial quantities of capital goods are not given, but are found by the model. I don't see why one would even argue here.

I don't think the comment above sets out Petri's impermanence problem very well. (I don't know what it means to talk about "the equilibrium path unfold[ing] in the real world".) The point is that markets only exist in the model at one point, before the beginning of time. Any time to reach equilibrium is too long. (This point is unoriginal.)

But I have no "'short-term' complaint" here about the model. I need not enter into any questions of whether or how Petri's impermanence problem is related to "realism".

I adopt a long run model so as to explain what Samuelson meant in part of his answer to Joan Robinson's question.

My point has nothing to do with indeterminacy, either. I even referred to "closing this model with utility-maximization". I believe some utility-maximizing closures can yield multiple equilibria and even a continuum of equilibria (indeterminancy). Other closures exist, perhaps with different properties. But this is neither here nor there to my point.

Nor am I complaining about the non-existence of aggregate capital in the model. (I don't see why the value of capital goods cannot be added up.)

But my anonymous commenter seems to think there is a valid "neoclassical theory of distribution". My point is that is that if such a beast exists, it is not the marginal productivity theory of distribution. The latter beast is as mythical as the unicorn.

I don't know why one would find unclear the meaning in my second paragraph in the last (fourth) part of this series of posts. I wrote: "Marginal productivity is not a theory of income distribution. I consider it an analysis, like the construction of the factor price frontier, of the choice of technique."

You wrote:

"I need not enter into any questions of whether or how Petri's impermanence problem is related to 'realism'."

Of course not. But you did enter it, and you made the incorrect claim that the problem is not related to the realism of the assumptions.

I was asking for clarification on this point because I thought your remarks about the "short-term" nature of intertemporal models was a complaint, a complaint which was supposed to justify why you're not criticizing a theory of distribution that neoclassical economists actually hold.

To the extent that you're just criticizing some claims of James Bates Clarck then I don't think there's any point of disagreement and in fact rigorous neoclassical theory has never claimed that marginal productivity is a theory of distribution.

Marshall wrote the following in 1890:

"This [marginal productivity] doctrine has sometimes been put forward as a theory of wages. But there is no valid ground for any such pretension."

If my impression that you were trying to criticize rigorous neoclassical theory was mistaken, then I don't think there are points of disagreement on this particular theme.

Anonymous says "But you did enter [into questions of whether or how Petri's impermanence problem is related to 'realism'], and you made the incorrect claim that the problem is not related to the realism of the assumptions." This, of course, is bollocks. I made no such claim.

Notice Anonymous does not state whether or not he agrees with me that "marginal productivity ... is an analysis, like the construction of the factor price frontier, of the choice of technique."

And I am not "just criticizing some claims of John Bates Clark" of only antiquarian interest.

Anonymous pretends Brad DeLong does not exist.

For that matter, Anonymous pretends that Marshall's claim that "[the marginal productivity] doctrine has sometimes been put forward as a theory of wages" is evidence that "rigorous neoclassical economi[sts?] [have] never claimed that marginal productivity is a theory of distribution", instead of suggesting the opposite.

Marshall says this in Book VI, Chap 1, Section 7 of his Principles. He does not provide any references, and he points out he is putting forth a partial equilibrium view in which, "in order to estimate net product, we have to take for granted all the expenses of the commodity on which he works, other than his own wages." Marshall also says that marginal productivity of labor "throws into clear light the action of one of the causes that govern wages." Somehow, I doubt Marshall is talking about the location of the so-called factor price frontier. In fact, Marshall holds the incorrect relative scarcity theory of value.

I suggested that your complaint that intertemporal equilibrium models are ‘short-term’ is one about realism and you answered by "My complaint is not one about 'realism' of assumptions."

If I misunderstood your answer above as referring to my specific inquiry then the fault is not entirely my own.

And it is only by being deliberately obtuse that you can interpret my claim that "rigorous neoclassical theory has never claimed that marginal productivity is a theory of distribution" as saying that there were no incompetent economists claiming otherwise -- indeed I even mentioned Clark.

But my claim that rigorous neoclassical theory has never contained the claim that marginal productivity theory is a distribution theory (in the sense of determining wages and interest) is perfectly sound.

I mentioned Marshall as specifically denying any such pretensions from marginal productivity theory (MPT) in 1890 -- and whatever one may think of his theories is irrelevant to this point.

Marshall was hardly alone in this -- indeed, the problem is finding competent neoclassical economists claiming otherwise.

P. Wicksteed wrote in 1894 that MPT is not a theory of the determination of wages.

"In this form [MPT] is not a law of distribution, but an

analytical and synthetical law of composition and resolution of industrial factors and products" (Essay on the Co-ordination of the Laws of Distribution)

Barone, who is sometimes credited with developing MPT earlier than Clark, although he published it only in 1896 also did not claim that MPT determines wages. Wicksell did not make such claims either.

G. Cassel wrote in 1918 that " marginal productivity itself is not an objectively ascertained factor in the pricing problem, but is in fact one of the unknowns in the problem...The statement that wages are determined by the marginal productivity of labour thus loses all independent meaning."

Later claims to the same effect are also easy to come by. "Please forget or disregard what John Bates Clark wrote about marginal productivity, and do not blame modern theorists for what our predecessors may have 'intended'. The intention of marginal productivity theories in modern theory is not the explanation of factor prices."

Fritz Machlup, "Reply to Professor Takata", Osaka Economic Papers, 1955

And of course, the "predecessors" who did make the mistake are not easily identifiable with the early neoclassical theorists either -- Clark seems to be the main culprit. Also note that "modern" in the above refers to 1955 -- half a century ago.

So not only is the proper domain of your criticism of antiquarian interest, but even in this restricted domain it can only be a criticism of the incompetence of particular individuals, not a criticism of neoclassical theory.

What an odd way of acknowledging that I never in this series of posts made a claim about whether or how the impermance problem is related to the realism of assumptions. And now Anonymous seems to be pretending, with his comments about "criticism of neoclassical theory", that I did not connect my posts up to instances of what some rigorous neoclassical economists (i.e., Walras) say. I explicitly said that my point "is [an] attempt to get clear the logic of the disaggregated model".

One might be more impressed with Anonymous' scholarship if he had a quote from a neoclassical author not to be found on Gonçalo Fonseca's page on the neoclassical theory of distribution.

Notice Anonymous does not state whether or not he agrees with me that "marginal productivity … is an analysis, like the construction of the factor price frontier, of the choice of technique." Nor does he comment on what Brad DeLong says neoclassical economists believe.

Perhaps I need to adopt a comment policy and to explore the technical means to enforce it.

Post a Comment