Paul Romer claims his 1990 model contains disaggregated capital:

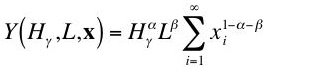

"The unusual feature of the production technology assumed here is that it disaggregates capital into an infinite number of distinct types of producer durables." -- Romer (1990):S80But he is mistaken. He gives the production function for final output as follows:

The first argument of the production function is the amount of human capital, strangely enough measured on a cardinal scale, employed in the manufacturing sector (as opposed to the research sector). The second argument is the amount of physical labor hired in the manufacturing sector. The remaining arguments are the quantities of the capital goods, each measured in numeraire units. That is, capital is measured in units of "foregone consumption". Apparently, Romer recognizes issues exist here:(1)

"It is possible to exchange a constant number of consumption goods for each unit of capital goods if the production function used to manufacture capital goods has exactly the same functional form as the production function used to manufacture consumption goods." -- Romer (1990): S81I saw that Romer (1990) was sensitive to a Cambridge capital critique, despite his erroneous claim to be representing capital as composed of diverse commodities, when I first read his paper several years ago. Kurz (2006) recently makes the same point, and apparently I want to see if Park (2006) has come out yet. Steedman (2003) criticizes the lackadaisical approach to measurement scale issues in new growth theory. So one's work can be lauded in mainstream economics, yet still contain technical flaws that were exposed long before and that invalidate one's results.

- Kurz, Heinz D. (2006). "Whither History of Economic Thought? Going Nowhere Rather Slowly?

- Park, M. (2006). "Homogenity Masquerading As Variety: The Case of Horizontal Innovation Models", Cambridge Journal of Economics (forthcoming)

- Romer, Paul M. (1990). "Endogenous Technological Change", The Journal of Political Economy, V. 98, N. 5 (Oct.): S71-S102.

- Steedman, Ian (2003). "On 'Measuring' Knowledge in New (Endogenous) Growth Theory", in Old and New Growth Theories: An Assessment (ed. by Neri Salvadori), Edward Elgar

No comments:

Post a Comment