|

| Figure 1: Rates of Profits for Switch Points for Differential Rates of Profits |

1.0 Introduction

Suppose one knows the technology available to firms at a given point in time. That is, one knows the techniques

among which managers of firms choose. And suppose one finds that reswitching cannot occur under this

technology, given prices of production in which the same rate of profits prevails among all industries.

But, perhaps, barriers to entry persist. If one analyzes the choice of technique for the

given technology, under the assumption that prices of production reflect stable (non-unit) ratios

of profits, differing among industries, reswitching may arise for the technology. The numerical

example in this post demonstrates this logical possibility.

The numerical example follows a model of oligopoly I have previously outlined. In some sense, the example is symmetrical to the example in this

draft paper.

That example is of a reswitching example under pure competition, which becomes an example without reswitching

and capital reversing, if the ratio of the rates of profits among industries differs enough.

The example in this post, on the other hand, has no reswitching or capital reversing under pure

competition. But if the ratios of the rates of profits becomes extreme enough, it becomes a reswitching

example.

2.0 Technology

The technology for this example resembles many I have explained in past posts.

Suppose two commodities, iron and corn, are produced in the example economy.

As shown

in Table 1, two processes are known for producing iron, and one corn-producing process is known.

Each column lists the inputs, in physical units, needed to produce one physical unit of the output for the industry for that column.

All processes exhibit Constant Returns to Scale, and all processes require services of inputs over a year to produce output of a single commodity available at the end of the year. This is an example of a model of circulating capital.

Nothing remains at the end of the year of the capital goods whose services are used by firms during the production processes.

Table 1: The Technology for a Two-Industry Model

| Input | Iron

Industry | Corn

Industry |

| Labor | 1 | 305/494 | 1 |

| Iron | 1/10 | 229/494 | 11/10 |

| Corn | 1/40 | 3/1976 | 2/5 |

For the economy to be self-reproducing, both iron and corn must be produced each year. Two

techniques of production are available. The Alpha technique consists of the first iron-producing

process and the lone corn-producing process. The Beta technique consists of the remaining

iron-producing process and the corn-producing process.

3.0 Price Equations

The choice of technique is analyzed on the basis of cost-minimization, with prices of production.

Suppose the Alpha technique is cost minimizing. Then the following system of equalities and

inequalities hold:

[(1/10)p + (1/40)](1 + rs1) + w = p

[(229/494)p + (3/1976)](1 + rs1) + (305/494)w ≥ p

[(11/10)p + (2/5)](1 + rs2) + w = 1

where p is the price of a unit of iron, and w is the wage.

The parameters

s1 and s2 are given constants, such that rs1

is the rate of profits in iron production and rs2 is the rate of profits

in corn production. The quotient s1/s2 is the ratio,

in this model, of the rate of profits in iron production to the rate of profits in

corn production. Consider the special case:

s1 = s2 = 1

This is the case of free competition, with investors having no preference among industries.

In this case, r is the rate of profits. I call r the scale factor for the

rate of profits in the general case where s1 and s2

are unequal.

The above system of equations and inequalities embody the assumption that a unit corn

is the numeraire. They also show labor as being advanced and wages as paid out of

the surplus at the end of the period of production. If the second inequality is

an equality, both the Alpha and the Beta techniques are cost-minimizing; this is

a switch point. The Alpha technique is the unique cost-minimizing technique if it

is a strict inequality. To create a system expressing that the Beta technique

is cost-minimizing,

the equality and inequality for iron production are

interchanged.

4.0 Choice of Technique

The above system can be solved, given s1, s2,

and the scale factor for the rate of profits. I record the solution for a couple

of special cases, for completeness. Graphs of wage curves and a bifurcation

diagram illustrate that stable (non-unitary) ratios of rates of profits can

change the dynamics of markets.

4.1 Free Competition

Consider the special case of free competition.

The wage curve for the Alpha technique is:

wα = (41 - 38r + r2)/[80(2 + r)]

The price of iron, when the Alpha technique is cost-minimizing, is:

pα = (5 - 3r)/[8(2 + r)]

The wage curve for the Beta technique is:

wβ = (6,327 - 9,802r + 3,631r2)/[20(1,201 + 213r)]

When the Beta technique is cost-minimizing, the price of iron is:

pβ = [5(147 - 97r)]/[2(1,201 + 213r)]

Figure 2 graphs the wage curves for the two techniques, under free competition

and a uniform rate of profits among industries.

The wage curves intersect at a single switch point, at

a rate of profits of, approximately, 8.4%:

rswitch = (1/1,301)[799 - 24 (8261/2)]

The wage curve for the Beta technique is on the outer envelope, of the wage curves,

for rates of profits below the switch point. Thus, the Beta technique

is cost-minimizing for low rates of profits. The Alpha technique is cost minimizing

for feasible rates of profits above the switch point. Around the switch point,

a higher rate of profits is associated with the adoption of a less capital-intensive

technique. Under free competition, this is not a case of capital-reversing.

|

| Figure 2: Wage Curves for Free Competition |

4.2 A Case of Oligopoly

Now, I want to consider a case of oligopoly, in which firms in different

industries are able to ensure long-lasting barriers to entry. These

barriers manifest themselves with the following parameter values:

s1 = 4/5

s2 = 5/4

In this case, the wage curve for the Alpha technique is:

wα = (4,100 - 4,435r + 100r2)/[40(400 + 259r)]

The price of iron, when the Alpha technique is cost-minimizing, is:

pα = (125 - 96r)/(400 + 259r)

The wage curve for the Beta technique is:

wβ = 8(126,540 - 195,289r + 72,620r2)/[160(24,020 + 9,447r)]

The price of iron, when the Beta technique is cost-minimizing, is:

pβ = 2(3,675 - 3,038r)/(24,020 + 9,447r)

Figure 3 graphs the wage curves for the Alpha and Beta techniques, for the

parameter values for this model of oligopoly. This is now an example of

reswitching. The Beta technique is cost minimizing at low and high rates

of profits. The Alpha technique is cost minimizing at intermediate rates.

The switch points are at, approximately, a value of the scale factor for

rates of profits of 12.07% and 77.66%, respectively.

|

| Figure 3: Wage Curves for a Case of Oligopoly |

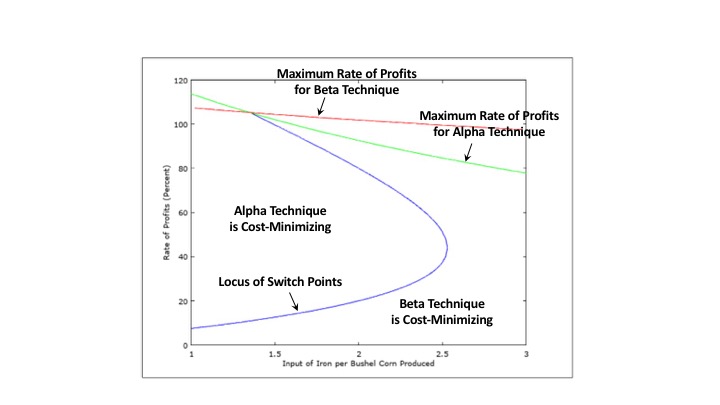

4.3 A Range of Ratios of Profit Rates

The above example of oligopoly can be generalized. I restrict myself to the case where the parameters expressing

the ratio of rates of profits between industries satisfy:

s2 = 1/s1

One can then consider how the shapes and locations of wage curves and switch points vary with continuous

variation in s1/s2. Figure 1, at the top of this post, graphs the

wage at switch points for a range of ratios of rates of profits. Since the Beta technique is cost-minimizing,

in the graph, at all high feasible wages and low scale factor for the rates of profits, I only graph the

maximum wage for the Beta technique. I do not graph the maximum wage for the Alpha technique.

As the ratio of the rate of profits in the iron industry to rate in the corn industry increases towards unity,

the model changes from a region in which the Beta technique is dominant to a reswitching example to an

example with only a single switch point. As expected, only one switch point exists when the rate of

profits is uniform between industries.

5.0 Conclusion

So I have created and worked through an example where:

- No reswitching or capital-reversing exists under pure competition, with all industries earning the same rate of profits.

- Reswitching and capital-reversing can arise for oligopoly, with persistent differential rates of profits across industries.

No qualitative difference necessarily exists, in the long period theory of prices,

between free competition and imperfections of competition.

Doubtless, all sorts of complications of strategic behavior, asymmetric information, and so on

are empirically important. But it seems confused to blame the failure of markets to clear

or economic instability on such imperfections.