Capital-reversing can arise in a couple of ways without reswitching. This post steps through a case in which positive price Wicksell effects can dominate negative real Wicksell effects. Around each switch point, firms choose to adopt a more capital-intensive technique of production for slightly lower interest rates. So real Wicksell effects agree, in this example, with the incoherent and outdated intuition of applied neoclassical economics. Nevertheless, due to the re-evaluation of a given set of capital goods at different interest rates, one can find a pair of points such that cost-minimizing firms adopt a more capital-intensive technique, from the given technology, at the higher interest rate. And this pair of points can span at least one switch point. Basically, I created a simple example to replicate graphs like those in Appendix D in Lazzarini (2011).

A case of a positive price Wicksell and negative real Wicksell effect is one case in my suggested taxonomy of Wicksell effects. Burmeister provides one possible neoclassical response to this sort of example. Burmeister advocated the use of David Champernowne’s (unobservable) chain-index measure of capital.

2.0 The Technology

Consider a very simple economy in which a single consumption good, corn, is produced. Entrepreneurs know of the two processes for producing corn shown in the last two columns of Table 1. One corn-producing process produces corn from inputs of labor time and steel. The other corn-producing process uses inputs of labor time and tin. The entrepreneurs know of two other processes, also shown in Table 1. Additional steel can be produced from inputs of labor time and steel. Similarly, labor time and tin can produce more tin.

| Inputs | Steel Industry | Tin Industry | CornIndustry | |

| Labor | 1 Person-Year | 1 Person-Yr | 1 Person-Yr | 2 Person-Yrs |

| Steel | 1/2 Ton | 0 Ton | 1/4 Ton | 0 Ton |

| Tin | 0 Kg. | 9/20 Kg. | 0 Kg. | 1/3 Kg. |

| Output: | 1 Ton Steel | 1 Kg. Tin | 1 Bushel Corn | 1 Bushel Corn |

All processes exhibit Constant Returns to Scale (CRS). Each process requires a year to complete. Their outputs become available at the end of the year, and they totally use up their inputs of capital goods over the course of the year.

3.0 Quantity Flows

Two techniques are available for producing a bushel of corn as net output.

The first technique, to be called the steel technique, operates the first process to produce 1/2 ton steel and the first corn-producing process to produce one bushel corn. 1/4 ton of the output of the steel-producing process replaces the steel-capital used up in producing steel. The other 1/4 ton output from the steel-producing process replaces the 1/4 ton steel used up in producing corn. In effect, 1 1/2 person-years labor are used in the steel technique for each bushel corn producing in a self-sustaining way.

In the tin technique, 20/33 kilograms tin are produced with the tin-producing process, and one bushel corn is produced with the second corn-producing process. 2 20/33 person-years labor are used in the tin technique for each bushel of corn in the economy’s net output.

Note that the production of corn with the steel system provides more consumption per worker-year than is provided with the tin system. Under the false and exploded neoclassical theory, one would expect the steel system to require more capital per worker. One would also expect it to be adopted at a low interest rate, since the low interest would be signaling a relative lack of scarcity of capital.

4.0 Price Equations

Next, I consider constant prices consistent with the adoption of each technique. Firms will not adopt a technique unless the interest rate (also known as the rate of profits) is earned for each process in use in a technique. For definitiveness, I assume that wages are paid at the end of the year out of output and that a bushel corn is the numeraire.

4.1 Steel Technique

Given these assumptions, the following system of two equations must hold when the steel technique is in use:

(1/2)ps(1 + r) + w = ps

(1/4)ps(1 + r) + w = 1where ps is the price of a ton of steel, w is the wage, and r is the interest rate.

Above is a system of two equations in three variables. This system has one degree of freedom. Two variables can be found as functions of the one remaining variable. For example, the wage and the price of steel can be expressed as (rational) functions of the rate of profits. And that price of steel can be used to find the value of capital. The resulting capital-output ratio is:

vs(r) = 2/(3 - r)where vs is the ratio of the value of capital to the value of output in the steel technique.

4.2 Tin Technique

The following system of two equations must hold when the tin technique is in use:

(9/20)pt(1 + r) + w = pt

(1/3)pt(1 + r) + 2 w = 1where pt is the price of a kilogram of tin.

The ratio of the value of capital to the value of output in the tin technique, vt, expressed as a function of the interest rate, is:

vt(r) = 200/(473 - 187 r)

5.0 Choice of Technique

The trade off between the wage and the rate of profits, for a given technique, is the wage curve for that technique. Figure 1 shows the wage curves for the two techniques, as well as the wage frontier formed as an outer envelope of the wage curves for all the techniques that comprise the technology. Given the interest rate, the cost-minimizing firm adopts the technique whose wage curve is on the frontier at that point. At the switch point, two techniques are simultaneously cost minimizing.

|

| Figure 1: The Wage-Rate of Profits Frontier |

The wage curve for a given technique expresses the wage as a function of the rate of profits. The rate of profits at which the switch point occurs is found by equating the wage for two techniques. In the numerical example analyzed in this post, the following quadratic equation arises:

(41/240)(1 + r)2 - (13/15)(1 + r) + 1 = 0The switch point occurs at a rate of profits of approximately 77.46%.

6.0 Conclusion

The above analysis has shown for the example:

- Which technique is cost-minimizing at any given interest rate up to a maximum.

- The ratio of the value of capital to output for each technique for each interest rate.

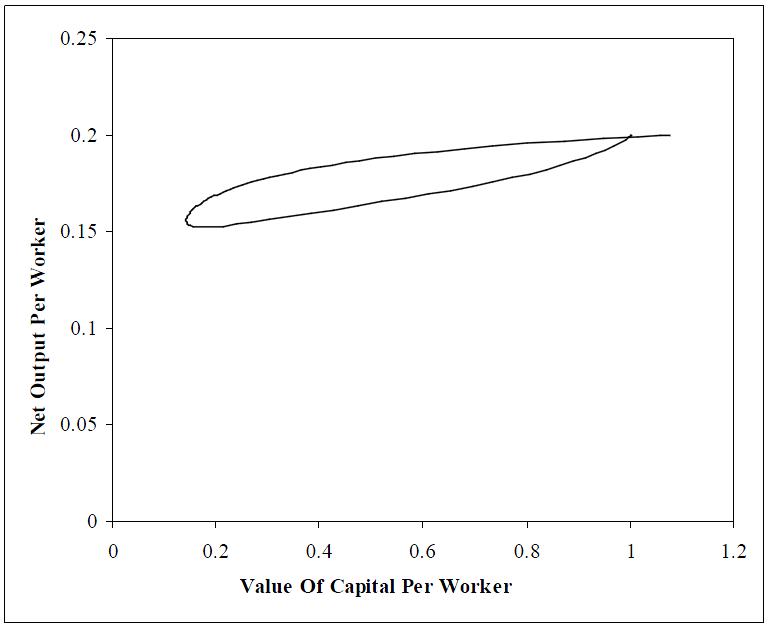

|

| Figure 2: The Rate of Profits Versus Capital-Intensity |

This example has shown that capital-reversing can exist around a switch point even in the absence of reswitching.

References

- Edwin Burmeiser (1980). Capital Theory and Dynamics, Cambridge University Press.

- Andrés Lazzarini (2011). Revisiting the Cambridge Capital Theory Controversies: A Historical and Analytical Study, Pavia University Press.